Understanding the latest secondary smartphone market trends 2026 is now essential, as the “brand-new-only” enterprise mindset is officially dead. Over the last several years, structural shifts in supply chains have forced an unprecedented corporate pivot toward circular, pre-owned hardware.

In 2026, corporate IT buyers face a harsh hardware reality. Driven by a severe global memory crisis, primary smartphone wholesale prices have jumped by double digits, effectively pricing out budget-conscious entry-level fleets. The era of cheap corporate upgrades is over—making the secondary smartphone market no longer a green alternative, but a financial necessity.

✓ < 1% Hardware Return Rate

✓ Ready-to-Ship Enterprise Inventory

For over a decade, IT procurement strategy followed a highly predictable, almost rhythmic blueprint. Every two to three years, corporate technology leaders would initiate a massive hardware refresh. They would buy brand-new mobile fleets directly from Original Equipment Manufacturers (OEMs) or tier-one carriers, deploy them to employees with fresh service contracts, write off the depreciation, and repeat the cycle.

In this legacy framework, refurbished devices were rarely considered. They were viewed as the domain of secondary consumer markets, lacking the structural guarantees, reliable logistics pipelines, and high-volume consistency required for enterprise-grade deployments.

Today, that blueprint is obsolete.

We are living through what economists are calling the “Great Tech Flip.” The classic “brand-new-only” corporate mindset is undergoing an unprecedented structural transition. High-quality, certified pre-owned (CPO) hardware has transformed from a fringe budgeting alternative into a core boardroom strategy.

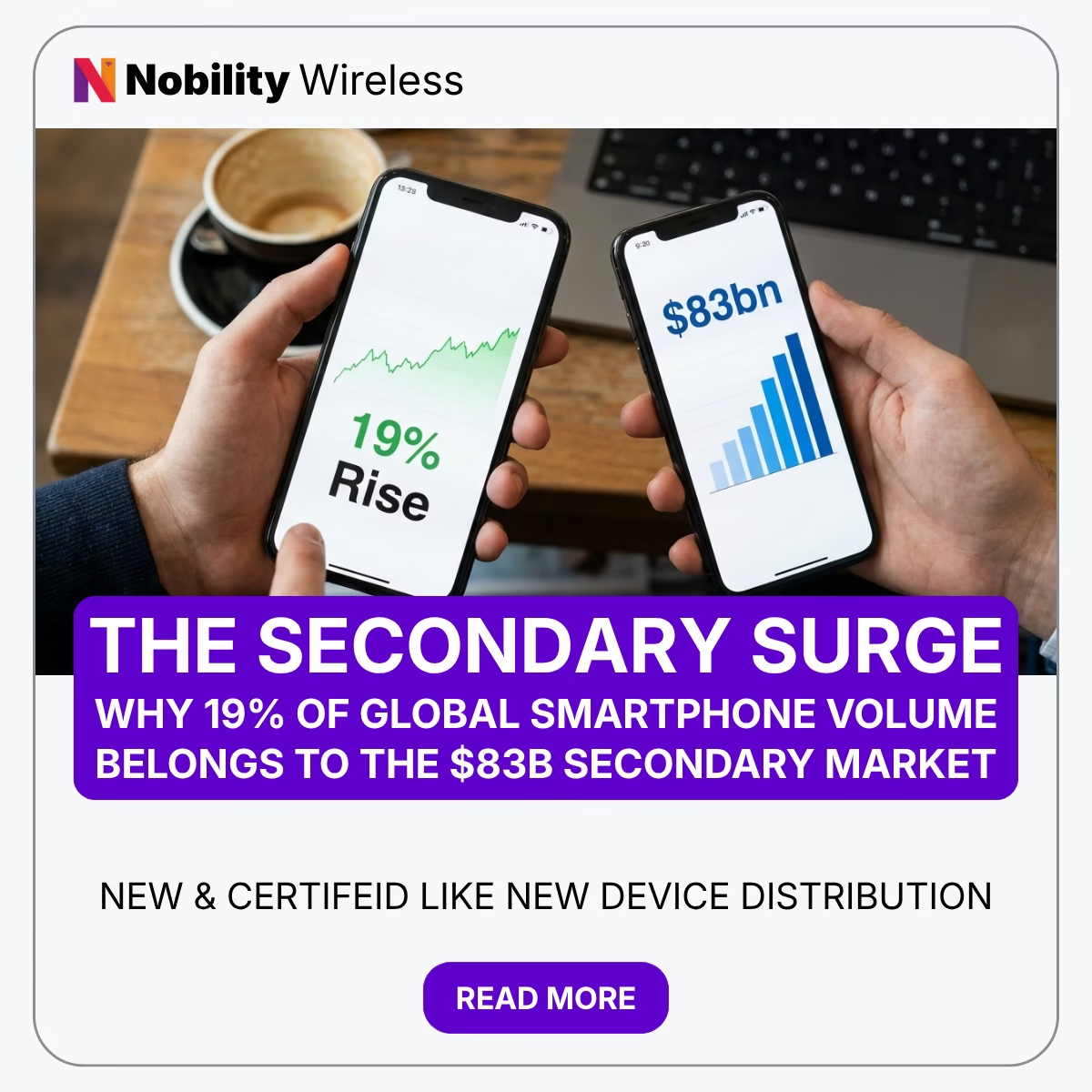

According to consolidated industry data from the International Data Corporation (IDC), the global secondary smartphone ecosystem has officially swelled to an $83.74 Billion powerhouse. More tellingly, pre-owned hardware now commands a staggering 19% share of all global smartphone volume.

At the same time, the primary market for brand-new devices has experienced its steepest contraction in historical terms. New smartphone shipments collapsed by -13.9% year-on-year, driven by a brutal combination of compounding supply shortages and soaring component prices.

For enterprise buyers, IT directors, and chief financial officers, this isn’t merely a temporary supply chain blip. It represents a permanent, structural shift in the economics of enterprise technology.

Part 1: Anatomy of the Primary Squeeze

To understand why enterprises are pivoting so aggressively to the secondary market, we must first look at the factors strangling the primary hardware market. The historical contraction in global new smartphone shipments is not a failure of consumer or corporate demand. It is a structural supply crisis.

1. The 300% Memory Price Spike & BOM Crisis

At the center of the primary hardware slowdown is an acute memory component deficit. Over the past year, memory costs skyrocketed by nearly 300%. For hardware manufacturers, memory and NAND flash storage are no longer minor line items; they now account for 65% of the total Bill of Materials (BOM) at the entry-to-mid tier level.

This pricing volatility has fundamentally shattered the unit economics of producing lower-cost and mid-range enterprise smartphones. The sub-$200 smartphone segment—which traditionally served as the backbone for high-volume enterprise deployments (such as field-force operations, logistics, retail, and construction)—has become economically unviable for major manufacturers to sustain. When component parts swallow up almost two-thirds of the manufacturing budget, entry-level devices cannot be built profitably.

2. Record-High Average Selling Prices (ASP)

Because OEMs cannot absorb these massive component spikes, they have shifted their manufacturing lines away from budget tiers. Instead, they are concentrating production on premium, high-margin flagship lines.

This strategic shift has driven the global average selling price (ASP) of new smartphones to a record-high $550—an increase of $100 in just twelve months. While consumer segments are feeling this price pinch, the impact on enterprise procurement budgets is magnified tenfold.

When a company needs to provision a fleet of 5,000 devices for a remote field crew or a corporate logistics team, a $100-per-unit premium translates to a $500,000 budget deficit.

3. Geopolitical and Logistics Pressure

Adding fuel to the fire, macro-economic tensions and transport blockades have added severe layers of cost pressure to primary hardware distribution. Escalating shipping fees, fuel surcharges, and raw materials costs have forced OEMs to reduce overall volume output, raise retail prices, and accept longer production lead times.

For corporate buyers, this means that even if they are willing to pay a premium for new devices, they are frequently met with delivery back-orders of 8 to 12 weeks. In the fast-moving business landscape, a two-month delay on field-force hardware translates directly to lost operational productivity and derailed deployment timelines.

The Global Hardware Landscape: Primary vs. Secondary Markets

To contextualize this transition, the table below highlights the divergent trajectories of the primary (new) and secondary (used/refurbished) global hardware markets:

| Market Metric | Primary Market (Brand New) | Secondary Market (Pre-Owned) | Enterprise Implications |

|---|---|---|---|

| Market Growth Rate | -13.9% Decline | +112% Growth | Demand is shifting directly to circular tech loops. |

| Average Unit Cost | $550 (Record-High ASP) | $255.68 (Avg. Value) | Enterprises save between 40% and 55% per fleet. |

| Estimated Total Value | $35 Billion | $83.74 Billion | The secondary market has surpassed new retail in liquid assets. |

| Lead Time / Availability | 8 to 12 Weeks (Backorder) | Immediate (Stock-Ready) | Pre-owned eliminates downtime on workforce deployments. |

| Carbon Impact (Per Device) | 85kg CO2e Generated | 64kg CO2e Avoided | Deploying refurbished tech instantly scores ESG points. |

Part 2: The Secondary Smartphone Market Trends 2026 — Anatomy of an $83B Ecosystem

While the primary hardware pipeline is constricted, the secondary market is enjoying a golden era of growth. These shifts are heavily driving the latest secondary smartphone market trends 2026. The transition of 19% of the world’s smartphone volume into pre-owned channels is being propelled by three key pillars:

1. The Financial Arbitrage of Refurbished Tech

The first and most obvious driver is financial. High-quality pre-owned devices—typically models that are only 8 to 12 months behind the current flagship release cycle—are trading at 40% to 55% discounts compared to their brand-new counterparts.

For an enterprise looking to deploy premium, secure operating systems (like iOS or high-end Android enterprise editions), this represents massive capital expenditure savings.

Through secondary acquisition channels, procurement teams can source certified pre-owned premium devices for less than the cost of a brand-new, compromised lower-end mid-tier device.

2. The Legitimacy of Manufacturer-Backed Certification

Historically, the primary barrier to enterprise pre-owned adoption was risk. IT departments feared receiving devices with degraded batteries, worn screens, outdated firmware, or unvetted histories.

That risk has been systematically dismantled by the rise of institutionalized, professionalized grading and refurbishment frameworks.

Major manufacturers and high-volume third-party logistics firms have established rigorous diagnostics workflows. Devices are completely disassembled, components are tested against strict baseline OEM specs, batteries are replaced if health falls below 85-90%, and the operating system is clean-flashed with the latest security updates. Many of these certified pre-owned devices now ship with comprehensive, enterprise-grade warranties, putting them on par with new out-of-the-box hardware.

3. Sustainable and Circular Procurement

Corporate sustainability mandates are no longer secondary public relations goals; they are compliance-driven boardroom directives. Major enterprises worldwide are bound by strict carbon reduction targets, Scope-3 emissions guidelines, and Extended Producer Responsibility (EPR) regulations.

The environmental math behind smartphone manufacturing is clear and sobering: Sourcing raw materials and manufacturing a single new smartphone generates roughly 85 kilograms of CO2 emissions. It consumes over 240 liters of water and requires extracting 80 kilograms of raw geological materials.

By choosing to deploy certified refurbished smartphone fleets, enterprises immediately extend the useful lifespan of existing hardware by an average of 3 to 5 years. This simple pivot effectively zeroes out the hardware’s manufacturing carbon footprint for the acquiring enterprise, making it one of the fastest, most measurable ways for an IT department to contribute to corporate net-zero targets. According to third-party studies conducted by Greenly and Alchemy, opting for a certified pre-owned smartphone avoids an average of 64kg of CO2 emissions per device.

🛑 “Refurbished” Doesn’t Mean “Risky”

For enterprise fleets, hardware consistency is everything. When sourcing secondary inventory, the difference between a high-performing deployment and a logistical nightmare comes down to standardized testing:

- 35-Point Diagnostics: Every B2B device must pass rigorous diagnostics verifying screen sensitivity, cellular band connectivity, battery life (85%+ health thresholds), and clean IMEI logs.

- Zero-Touch MDM Enrollment: Out-of-the-box software compatibility (Apple DEP/Android zero-touch) must be cleared and reset at the hardware level so your IT team can deploy securely.

Part 3: Why This Pivot is Permanent

Some industry observers wonder: Will corporate procurement return to 100% brand-new fleets once the global memory crisis resolves and supply chains stabilize?

The consensus among market analysts is no. The structural advantages of the secondary market have reshaped buyer expectations, and the shift is here to stay.

1. The Flattening of the Smartphone Innovation Curve

There was a time when a two-year-old smartphone felt functionally obsolete. In the early-to-mid 2010s, each new smartphone generation introduced massive, revolutionary leaps in processor speed, display technology, and network capability (such as the jump from 3G to 4G LTE). IT departments had to buy new to keep their applications running smoothly.

That curve has flattened.

Today’s flagships and mid-tier devices are so highly engineered that the year-over-year performance gains are incremental rather than revolutionary. A smartphone released twelve, eighteen, or even twenty-four months ago possesses more than enough processing power, RAM, and camera capability to run any enterprise app—from field-force logistics tools to secure database-connected field software.

Because the practical utility of older devices has remained remarkably high, there is very little operational benefit to paying premium pricing for nominal, next-generation incremental updates.

2. The Maturation of Trade-In Infrastructure

The secondary market is supported by a highly efficient, automated trade-in engine. Carriers, electronics retailers, and direct-to-consumer manufacturers have built highly frictionless trade-in portals that capture used devices at a massive scale.

According to the newest trade-in report by CCS Insight and Alchemy, US consumers alone are holding on to an estimated $83.74 Billion in unrealized trade-in value from unused devices sitting in households. This means the flow of top-tier consumer tech back into commercial circular loops is hitting historic volumes. This influx of devices is reshaping secondary smartphone market trends 2026 by securing a consistent, graded supply chain. Instead of old phones sitting forgotten in desk drawers, they are fed directly into institutional refurbishment pipelines. This highly reliable, predictable inflow ensures that high-volume enterprise suppliers always have a steady, graded, and certified inventory to support rapid enterprise deployments.

Part 4: Your Actionable Enterprise Blueprint

Navigating these secondary smartphone market trends 2026 and transitioning your corporate fleet procurement toward a secondary-first strategy doesn’t mean compromising on security, reliability, or ease of deployment. It simply requires replacing your legacy procurement channels with a modern, circular model.

Here is a step-by-step blueprint for transition:

Step 1: Audit Your Operational Requirements

Not all roles within your organization require the same hardware profile.

- Tier 1 (Premium Users): Executive teams or specialized software engineers may require high-end, current-generation flagships.

- Tier 2 (General Workforce): Operations, administration, and sales divisions are prime candidates for high-grade certified pre-owned smartphones that are 12 to 18 months behind the release cycle.

- Tier 3 (Field, Warehouse & Logistics): Ruggedized, certified pre-owned mid-tier devices can be deployed in bulk, saving up to 55% on upfront hardware costs.

Step 2: Establish a Standardization Protocol

Work with a trusted enterprise logistics partner like Nobility Wireless to standardize on specific, vetted models. Standardizing your pre-owned deployments ensures that your IT department can easily manage device profiles, push centralized mobile device management (MDM) configurations, and easily source matching accessories (such as cases, screen protectors, and vehicle docks) in bulk.

Step 3: Integrate Certified Pre-Owned into Your MDM

Modern Mobile Device Management (MDM) tools like Microsoft Intune, MobileIron, or Apple Business Manager operate identically regardless of whether a device is brand-new or certified refurbished. By working with an authorized enterprise partner, your certified pre-owned fleets can be pre-enrolled at the distributor level.

When your employees unbox their pre-owned devices, the phones will automatically connect to your network, pull down your security policies, and install your corporate app suite—delivering a zero-touch, seamless provisioning experience.

Part 5: The Nobility Wireless Advantage

At Nobility Wireless, we have spent years engineering a logistics and device-provisioning infrastructure that eliminates the traditional friction points of pre-owned corporate deployments. We don’t just supply devices; we deliver complete, end-to-end operational readiness.

- Zero-Defect Quality Control: Every device that enters our warehouse is put through a rigorous multi-point physical and hardware diagnostics process. We verify battery chemistry, screen sensitivity, ports, antennas, and processing units. When your shipment arrives at your facility, every device is 100% certified and ready for field deployment.

- Frictionless Supply Channels: We maintain highly deep, diverse stockpiles of graded enterprise devices. By bypassing the traditional OEM backlog and avoiding the primary manufacturing squeeze, we can fulfill high-volume deployments in days rather than months.

- Complete Lifecycle Support: From active deployment and MDM provisioning to secure asset disposition, repair, and circular trade-ins, we handle your devices’ entire operational lifecycle. We help you extract maximum value out of your technology budgets, reduce your electronic waste footprint, and scale your business with zero operational drag.

Conclusion: The New Way Forward

The global macroeconomic shifts of 2026 have drawn a clear line in the sand. The days of paying premium, inflated prices for minor year-over-year tech improvements are over.

With new shipments down by -13.9% according to the IDC Mobile Tracker and the secondary trade-in market surging past $83 Billion, the numbers make the decision for you. Circular hardware procurement is no longer a niche cost-saving experiment; it is the modern standard for agile, cost-effective, and environmentally responsible enterprise operations.

Optimize Your Fleet Logistics & Save Up to 55%

Stop waiting on long OEM lead times and overpaying for nominal updates. Let’s build a secure, sustainable, and cost-effective mobile hardware strategy tailored to your organization.